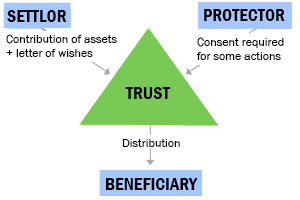

A trust is a legally created fiduciary arrangement designed for the security, growth, and division of assets. There are three distinct roles in a trust, with countless combinations of trust parties. A trust can be created by one person or many, it can be managed by anyone the founders choose, and it can benefit a specific person or group of people. Each role comes with different responsibilities and expectations that must be followed for the trust to succeed and be respected as the legal owner of its assets.

The Role of the Grantor/Settlor/Creator

The grantor (also known as the creator or settlor) is the owner of the property and assets who creates the trust and transfers the assets to the trust. Grantors create trusts (by executing a trust agreement) with the intent to hold the property and assets on behalf of and for the benefit of another party (the beneficiary). The grantor can place various types of assets into the trust, such as:

- Real estate

- Vehicles

- Investments

- Bank account funds

- Personal property, such as family heirlooms, antiques, and art

- Businesses

Essentially, the grantor can place anything they own into the trust.

Grantors may be liable for paying a gift tax based on the value of the assets they place into the trust. The amount owed will vary based on the type of trust the settlor creates.

The grantor has another essential role to perform: determining who will benefit from the assets. Legally, the grantor must select a specific person or group of people. Most of the time, grantors set up trusts to benefit their heirs, but they can also designate entities like churches or charities.

Trusts can be either revocable by the grantor or irrevocable.

Revocable Trusts and the Grantor Role

In a revocable trust, grantors often retain control of the trust and its assets and may make changes to the trust throughout their lifetime, both to assets and trustees. The grantor of a revocable trust can cancel the trust at any point, change the beneficiaries, and make other substantial changes. At the time of the grantor’s death, the trust becomes irrevocable, and if the grantor was also the trustee during their lifetime, a successor trustee identified in the trust agreement takes control according to the rules laid out in the state code.

Irrevocable Trusts and the Grantor Role

An irrevocable trust, on the other hand, cannot be modified, even by the grantor. In this case, the grantor transfers assets to the trust, selects a trustee, names the beneficiaries, and constructs a trust agreement to ensure wishes are carried out. From there, the grantor has no obligations or duties until they need to add assets per the trust agreement.

Irrevocable trusts can be changed by court order or with the consent of all parties.

The Role of the Trustee

The next party to enter the picture is the trustee. This person will oversee and administer the trust going forward. Trustees are named by the grantor to care for the assets of the trust. Often, trustees are compensated for their time and services from the trust’s funds.

Trustees hold a lot of power when it comes to managing the trust. Essentially, the trustee has the right to do whatever is necessary to protect and grow the trust’s assets. In a way, the trustee runs the trust like a business. They can take almost any income-generating action to grow the trust’s worth. For example, a trustee can:

- Enter into real estate agreements on behalf of the trust

- Make investments with trust assets, including cash

- Generate income by renting out valuables from the trust

- Raise money through donations and gifts

While the trustee has a significant amount of leeway in how they handle trust funds, there are specific requirements trustees must meet. There are also repercussions for mishandling trust assets. If the trust loses money due to mismanagement or recklessness, the trustee is personally liable and must repay the trust.

A trustee remains in charge of the trust until the funds are exhausted, or the trustee is removed in a legal proceeding. If a trustee dies, the grantor will need to designate someone new to manage the trust.

Revocable Trusts and the Trustee Role

When the grantor is the trustee, they can make any changes they want.

However, when the trustee is a third party, they must follow the trust agreement and fiduciary duties under state law, but can be removed or changed by the grantor. Upon the death of the grantor, the trust becomes irrevocable and the trustee role transforms accordingly.

Irrevocable Trusts and the Trustee Role

The trustee typically has complete control over an irrevocable trust, subject only to the trust agreement and their fiduciary duties under state law.

The Role of the Beneficiaries

Beneficiaries “benefit” from the trust. In other words, they are entitled to the trust’s assets, as directed by the trust agreement and controlled by the trustee. Many times, there are multiple beneficiaries—the trust should address asset division ahead of time. Beneficiaries have two roles:

- They receive payments from the trust and pay the associated taxes.

- They can audit the trust annually to verify that the trustee is handling the trust responsibly. They can also demand accounting oversight.

Beneficiaries have several legal rights related to the trust. For example, they can seek to have a trustee removed if the trustee mismanages the trust. Examples of mismanagement include behaviors like spending the funds inappropriately, making reckless investments, or failing to log and record how they have spent funds.

When a trustee is removed, the beneficiaries are responsible for replacing them.

The Costs Associated With Setting Up A Trust

A trust is created by signing a trust agreement with the trustee and then transferring property into the name of the trust (which is referred to as funding the trust). A trust does not exist until property is actually transferred into it, even if a trust agreement is signed. It does not take a long time to form a trust – only as long as it takes to draft and sign a trust agreement and then complete the necessary steps (usually the completion of paperwork) to transfer the property into the trust’s name. A trust can cost anywhere from a few hundred dollars to thousands of dollars in legal fees, depending on the complexity of the trust agreement’s terms and the type and amount of property to be transferred into the trust. “The Parties Involved In A Trust” is discussed in more detail in my book “Nothing But The Truth About Estate Planning, Probate And Living Trusts”. Download your copy today.